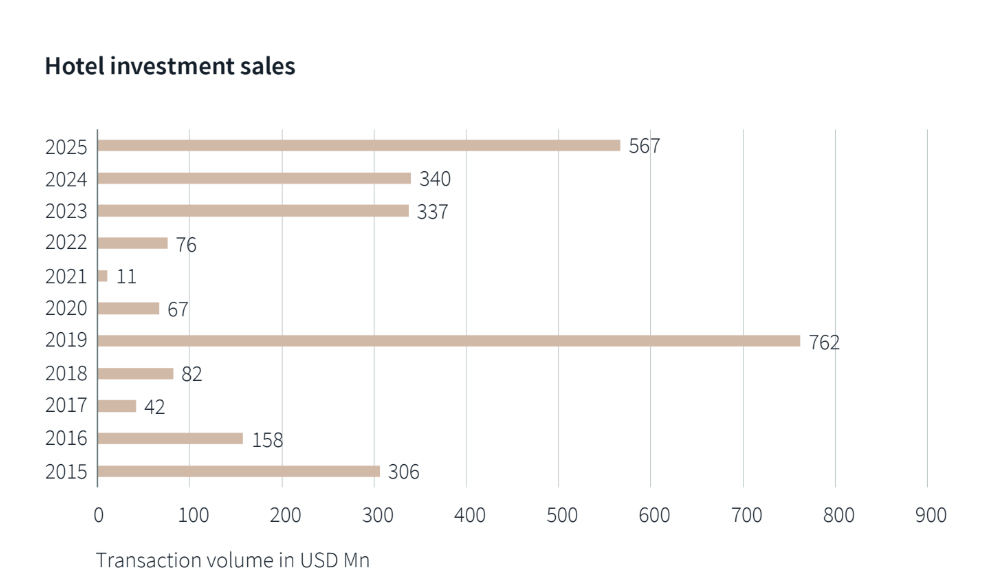

JLL reports India’s hotel investment market surged 67% in 2025 to USD 567 million, driven by institutional capital, operational hotel assets and strong Tier II and III city activity.

India’s hotel investment market reached approximately USD 567 million across 28 transactions in 2025, recording a 67 per cent increase over USD 340 million in 2024, according to JLL.

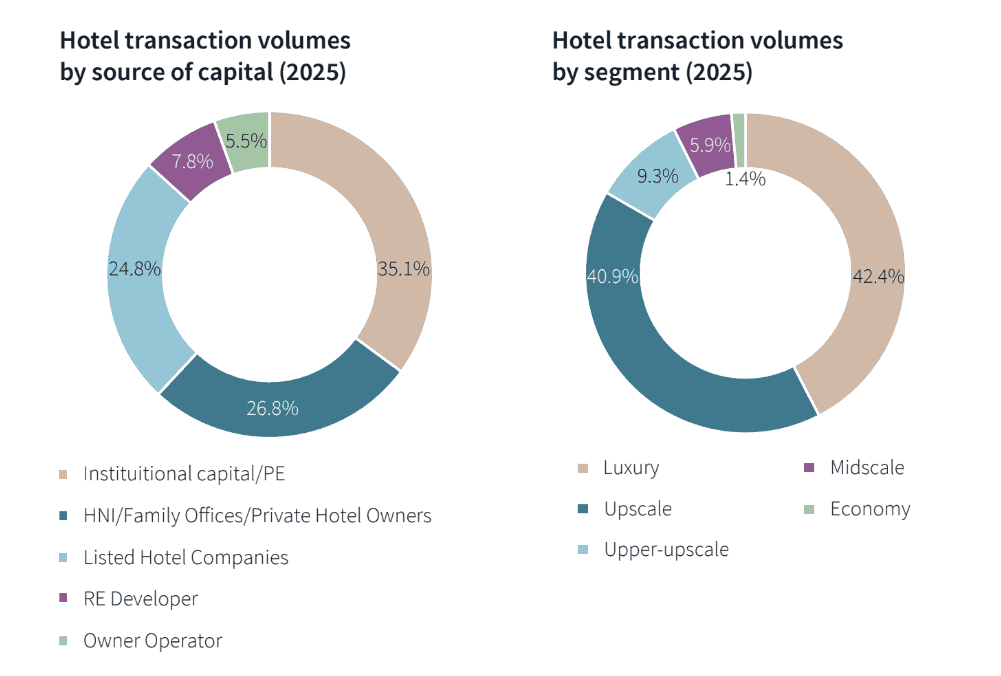

Institutional capital and private equity firms led transaction activity, accounting for 35 per cent of total volume. High net-worth individuals, family offices and private hotel owners accounted for 27 per cent, followed by listed hotel companies at 25 per cent. Real estate developers contributed 8 per cent, while owner-operators accounted for 5 per cent.

Tier II and III cities accounted for approximately 40 per cent of total transaction volume, continuing the momentum seen in the previous year. These markets included luxury resorts in Rishikesh, upper-upscale properties in Goa, and upscale to midscale properties across emerging urban centres such as Ludhiana, Nashik, Vadodara, Udaipur and Lonavala.

Gaurav Sharma, Managing Director, Hotels, India & Senior Director, Hotels Capital Markets, Asia, said, “India’s hotel investment market is reflecting a clear step-up in both investor confidence and market depth, with rising transaction activity supported by a broader mix of institutional and domestic capital. What is particularly encouraging is the continued expansion beyond gateway cities, with Tier II and III markets steadily evolving into more mature, investment-grade destinations backed by improving operating performance and scalability. This shift is meaningfully expanding the investable universe and enabling more strategic capital deployment across geographies.”

“The momentum has carried strongly into 2026, with a robust start to the year underscoring sustained capital appetite. Beyond volumes, we are seeing increasing sophistication in how capital is being deployed, through platform-led strategies and institutional partnerships, signalling a more mature and organised investment landscape. At the same time, strong asset performance has introduced a degree of supply-side discipline, with high-quality hotels being tightly held, making available opportunities more selective and highly sought after,” he added.

He also said, “Looking ahead, a supportive policy environment, including land monetisation initiatives and tourism-led infrastructure development, is expected to unlock new avenues for investment. While external uncertainties remain a factor to watch, the underlying drivers, resilient domestic demand, infrastructure expansion, and diversified capital sources, provide a strong foundation for continued growth. We expect this to translate into higher transaction activity through the year, with more assets coming to market and increased participation from institutional investors, reinforcing India’s position as a compelling hospitality investment destination.”

Beyond hotel transactions, 2025 also saw institutional capital deployment for consolidation and strategic partnerships totalling approximately USD 125 million. The report also noted that strong operating performance has reduced the availability of tradeable assets, as owners continue to retain high-performing properties. This has made premium hotel assets more selective in the transaction market.

Operational hotels lead transaction activity

Operational hotels accounted for 69 per cent of total transaction volume in 2025. Under-construction or non-operational properties accounted for 18 per cent, while land transactions, including leases, made up 13 per cent.

By segment, luxury properties accounted for the largest share of transaction volume at 42 per cent, followed by upscale properties at 41 per cent. Upper-upscale properties contributed 9 per cent, midscale properties 6 per cent and economy properties 2 per cent.

Branded hotel signings reached 51,647 keys across 424 Properties in 2025, a 23 per cent increase over the previous year. Around 71 per cent of these signings by key count were concentrated in Tier II and III cities.

Management contracts continued to dominate, increasing from 81 per cent in 2024 to 84 per cent in 2025. Franchise agreements remained at 14 per cent, while lease and revenue-share arrangements declined from 5 per cent to 2 per cent.

Greenfield development activity reached approximately 33,170 keys in 2025, surpassing 2024 by 17 per cent. Large-format hotels with more than 250 keys also recorded higher activity, with 29 signings in 2025 compared with 21 in 2024.

While large-format signings remained concentrated in Tier I markets such as Mumbai, Bengaluru, Hyderabad, Pune and Delhi, the format also expanded into markets including Guwahati, Visakhapatnam, Indore and Pushkar.

Investment activity continues into 2026

In the first quarter of 2026, hotel transaction volumes reached approximately USD 185 million, a 58 per cent increase over USD 117 million recorded in Q1 2025.

Notable activity included Warburg Pincus acquiring a 41 per cent stake in Fleur Hotels, a subsidiary of Lemon Tree Hotels, with a USD 107 million commitment for portfolio expansion. Other activities included operating hotel transactions, land monetisation deals and platform consolidation acquisitions.

The report noted that multiple factors are expected to influence hotel investment activity through 2026. These include liquidity among listed hotel companies, expected capital market entries by additional operators seeking portfolio expansion, and institutional capital and private equity funds looking at hotel portfolio acquisitions.

Government initiatives are also expected to create opportunities through land monetisation at airports and government-led auctions in strategic micro-markets such as Yashobhoomi, also known as IICC, Neopolis in Hyderabad, Fintech City in Chennai and Jewar Airport.

The FY 2027 tourism-focused budget is also expected to support hospitality demand and development through initiatives to develop 15 new cultural destinations around archaeological sites and transport infrastructure upgrades.

Goa was cited as an example of conversion activity, with independent and unbranded properties moving into established brand portfolios. Improved air services and road, rail and water infrastructure are expected to support the market’s continued growth as a leisure destination.

Branded hotel openings in 2025 stood at approximately 8,990 keys across 103 properties, with 64 per cent of keys concentrated in Tier II and III cities.

The report also noted that the tightening supply of credible tradeable hotel stock remains a factor to monitor. Strong operating performance is encouraging owners to retain high-performing assets, limiting the availability of premium properties. While this supports valuations, it may constrain transaction volumes if supply limitations continue.

Geopolitical uncertainties could affect international travel patterns and increase stock market volatility, potentially influencing investor sentiment. However, JLL said the domestic tourism focus of many investments provides some insulation from external shocks.

The report also pointed to a shift towards consolidation and platform-level investments, with strategic partnerships and entity-level capital deployment indicating a move beyond purely asset-level transactions.

Read More: News